Photo by Brett Sayles on Pexels

For decades, the telecommunications industry wrestled with a painful identity crisis: were carriers mere “dumb pipes,” or were they sophisticated technology companies capable of delivering differentiated value? The AI revolution may have finally settled that debate — but not in the way most executives originally hoped. The pipe, it turns out, is the product. And suddenly, everyone wants a piece of it.

AI Reframes the Infrastructure Investment Thesis

Artificial intelligence is driving a capital expenditure wave unlike anything the telecom industry has seen since the early 4G buildout era. But this cycle is different in character and scope. Rather than investment concentrated at the application or service layer, AI is pulling dollars down through the entire technology stack — from hyperscale data centers and long-haul fiber to access networks, distributed edge nodes, and industrial IoT connectivity.

The reason is architectural. Large language models, real-time inference engines, and AI-driven automation platforms are extraordinarily hungry for bandwidth, low-latency connectivity, and reliable, high-throughput transport. Training a frontier AI model requires massive data center interconnect (DCI) capacity. Deploying that model at the edge — where it can power autonomous vehicles, smart factories, or real-time network optimization — demands low-latency access networks and dense fiber backhaul. Every layer of the telecom stack suddenly has a starring role.

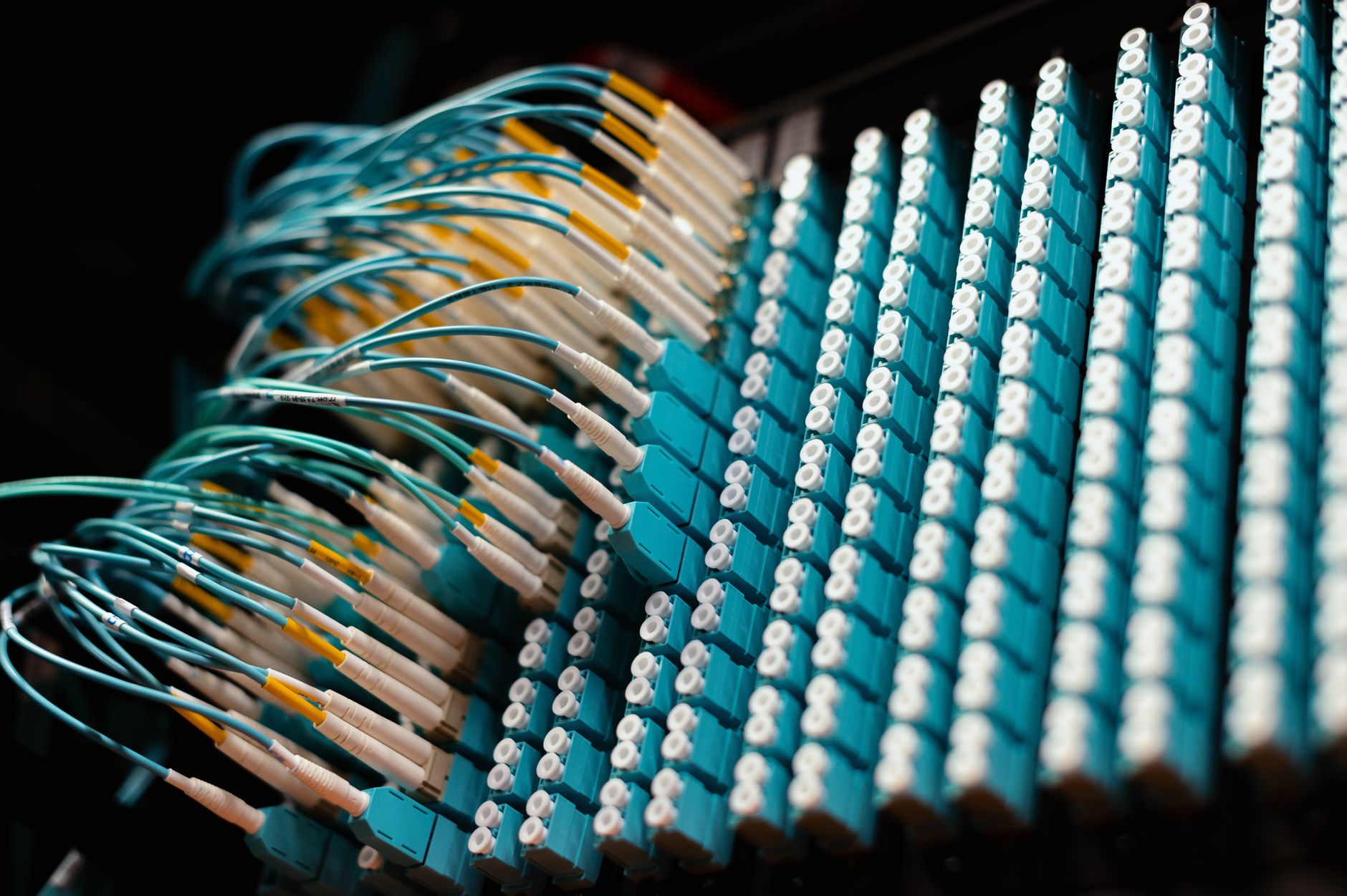

Fiber: The Foundation Everyone Is Scrambling For

If AI has a physical foundation, it is fiber. Hyperscalers like Microsoft, Google, and Amazon Web Services are aggressively leasing and, in some cases, building their own fiber routes to interconnect data centers at the terabit scale. Meanwhile, telecoms and neutral host providers are racing to capitalize, expanding dark fiber inventories and upgrading wavelength capacity on existing routes.

Data center interconnect spending is projected to grow significantly through the decade as AI clusters demand coherent optical transport capable of sustaining 400G, 800G, and eventually 1.6T wavelengths across metro and long-haul routes. For carriers with owned fiber assets — AT&T, Lumen, Zayo, and others — this represents a genuine monetization opportunity that pure software plays simply cannot replicate.

On the access side, fiber-to-the-premises (FTTP) deployment is accelerating not just for residential broadband but as the upstream pathway for AI-capable edge infrastructure. The BEAD program in the United States, with its $42.45 billion in federal funding, is adding policy tailwinds to a buildout that AI economics are already justifying on commercial grounds alone.

Edge Computing Gets Its Moment — For Real This Time

The telecom industry has been promising an “edge computing revolution” for years, often with limited commercial traction. AI inference workloads may finally deliver the use cases that justify distributed edge architecture at scale.

The logic is compelling: running AI inference in centralized cloud data centers introduces latency that is incompatible with time-sensitive applications. Autonomous industrial robots, real-time video analytics, connected vehicle coordination, and AI-assisted medical diagnostics all require sub-10ms response times that only edge-deployed compute can reliably provide. Carriers operating radio access network (RAN) infrastructure are uniquely positioned to host edge nodes co-located with baseband units and aggregation points.

Multi-access Edge Computing (MEC) deployments are evolving rapidly, with vendors like Ericsson, Nokia, and AWS Wavelength offering integrated platforms that allow application logic to run physically close to end users on carrier infrastructure. The commercial model — whether as a managed service, a platform fee, or infrastructure-as-a-service — is still being negotiated across the industry, but the technical case is increasingly airtight.

IoT and the Network as AI Sensor Grid

AI doesn’t just consume connectivity — it generates demand for sensing infrastructure. The Internet of Things, long a telecom buzzword with underwhelming monetization, is experiencing renewed investment momentum precisely because AI needs data, and IoT is how you collect it at scale.

Industrial IoT deployments on private 5G networks are feeding operational data into AI-driven predictive maintenance, quality control, and logistics optimization systems. LPWAN technologies like NB-IoT and LTE-M are gaining traction in smart city, agriculture, and utility metering applications where AI analytics add measurable ROI to previously passive sensor deployments.

Carriers are beginning to market their network infrastructure not just as a connectivity product but as a data-acquisition and edge-processing platform — a fundamental repositioning that could unlock new enterprise revenue streams.

The RAN Itself Becomes AI-Native

Perhaps the most profound shift is happening inside the network itself. Open RAN architectures are enabling AI-driven RAN Intelligent Controllers (RICs) to dynamically optimize spectrum allocation, interference management, and energy efficiency in ways that static, vendor-proprietary configurations never could. Network operators are deploying near-real-time RIC applications — called xApps and rApps — that use machine learning to continuously tune network performance at a granularity previously impossible.

This isn’t just operational efficiency. AI-native RAN represents a structural shift in how networks are built and operated, with software intelligence replacing hardware rigidity at the most critical layer of the wireless stack.

Industry Outlook: The Carriers Who Get This Will Win

The operators best positioned for the AI era are those that stopped apologizing for being infrastructure companies and started doubling down on it. Fiber assets, spectrum holdings, tower portfolios, and data center footprints — the “boring” plumbing of telecommunications — are now among the most strategically valuable assets in the technology sector.

The carriers that will struggle are those still searching for over-the-top service differentiation while underinvesting in the physical and logical infrastructure that AI-driven demand requires. In the age of artificial intelligence, the network isn’t the means to an end. For the telecom industry, the network is the end — and that changes everything.