Photo by Brett Sayles on Pexels

AI Workloads Are Rewriting the Rules of Digital Infrastructure

The artificial intelligence gold rush is no longer just a story about software algorithms and silicon chips — it is rapidly becoming one of the most transformative forces in the history of telecommunications infrastructure. As generative AI platforms, large language models (LLMs), and machine learning pipelines scale at breathtaking speed, the physical networks underpinning them are being pushed to their absolute limits. Optical fibre manufacturers, data centre operators, and network infrastructure companies are finding themselves at the very center of this seismic shift.

STL (Sterlite Technologies Limited), one of the world’s leading optical and digital solutions companies, has highlighted a clear and growing correlation between the AI boom and surging demand for high-capacity fibre connectivity and advanced data centre interconnects. The company’s assessment echoes a broader industry consensus: the compute-intensive nature of AI is fundamentally incompatible with yesterday’s network infrastructure.

Why AI Demands So Much More From Fibre Networks

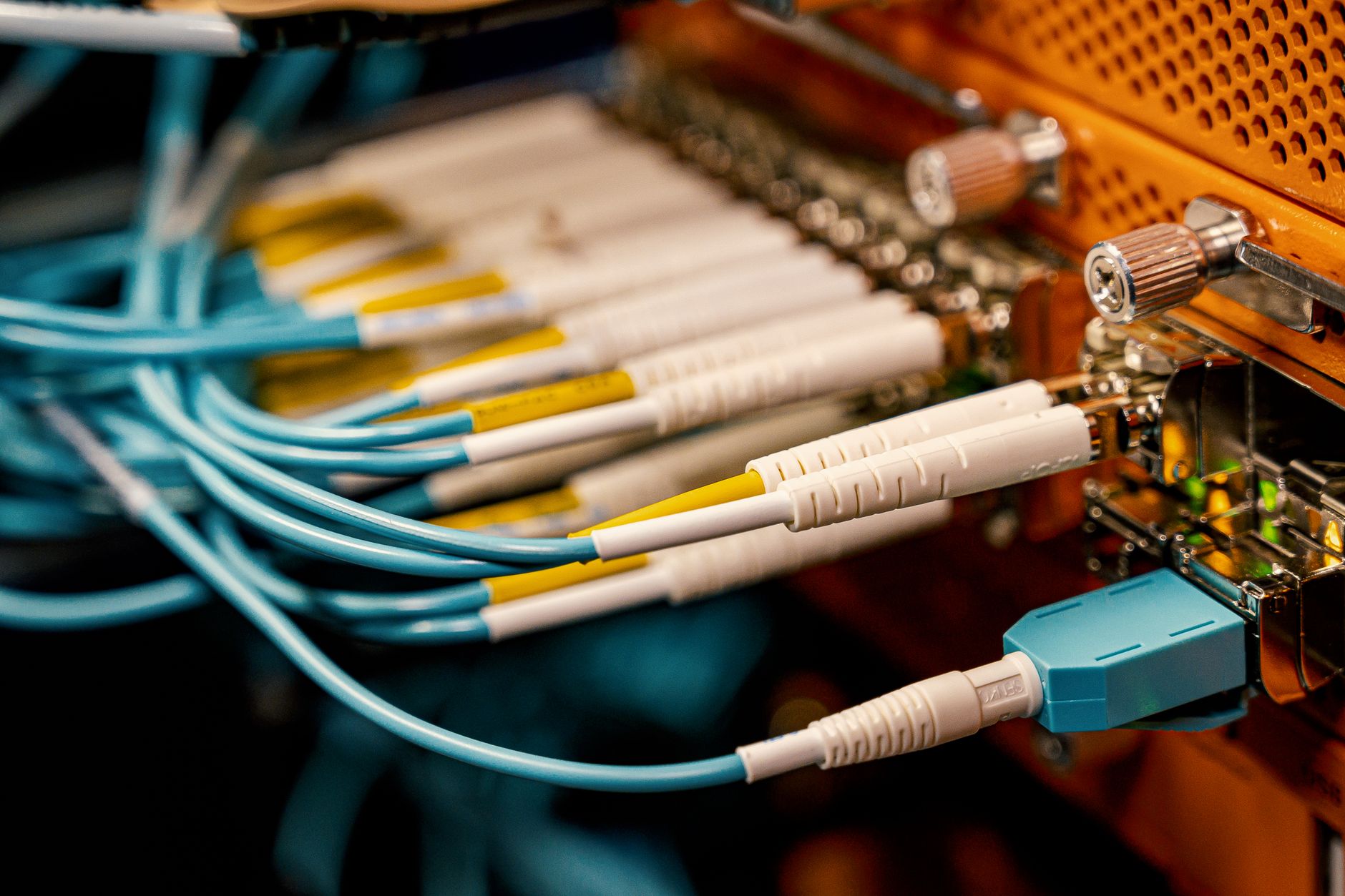

Training a single large language model like GPT-4 or Google’s Gemini requires moving petabytes of data across thousands of GPUs simultaneously. This process — known as distributed training — depends critically on ultra-low latency, high-throughput interconnects between servers, racks, and entire data centre campuses. Traditional copper-based or even early-generation fibre deployments simply cannot deliver the bandwidth density and signal integrity that modern AI clusters require.

Modern AI data centres are increasingly deploying 800G and even 1.6T optical transceivers, moving well beyond the 100G and 400G standards that dominated just a few years ago. Dense Wavelength Division Multiplexing (DWDM) technology is being pushed to new spectral efficiency frontiers, while coherent optical solutions are enabling data centre interconnects (DCI) that span hundreds of kilometres without signal degradation.

Intra-Data Centre vs. Inter-Data Centre Connectivity

The fibre demand story plays out on two distinct fronts. Inside the data centre, AI accelerator clusters — built around NVIDIA H100 and H200 GPUs, AMD MI300X chips, and custom silicon from the likes of Google (TPUs) and Amazon (Trainium) — require spine-leaf network architectures with massive parallel fibre runs. Industry analysts estimate that a single 100MW AI-optimised data centre can require millions of metres of fibre just for internal connectivity.

Outside the data centre walls, the challenge is equally daunting. Hyperscalers are building sprawling campus environments where multiple data centre buildings must communicate with near-zero latency. This is driving demand for dark fibre leasing, metro optical rings, and dedicated high-capacity terrestrial and subsea cable systems. STL and its peers are racing to meet this demand with next-generation single-mode fibre products designed for high-density, high-bend-tolerance deployments.

Market Numbers Tell a Compelling Story

The financial scale of this infrastructure buildout is staggering. Global data centre capital expenditure is projected to exceed $400 billion annually by 2027, with a significant and growing portion directed toward connectivity infrastructure rather than raw compute. Meanwhile, the global optical fibre and cable market — already valued at over $10 billion — is forecast to grow at a compound annual growth rate (CAGR) of approximately 10–12% through the end of the decade, directly fuelled by AI-driven demand.

Major cloud providers including Microsoft, Google, Amazon Web Services, and Meta have collectively committed hundreds of billions of dollars to data centre expansion through 2026 and beyond. Each of these facilities represents a major new anchor for fibre network deployments, pulling demand not just for long-haul connectivity but also for last-mile and middle-mile fibre builds in previously underserved regions where land costs support large-scale campus construction.

The Edge AI Factor

Looking beyond centralised hyperscale facilities, the emergence of edge AI is creating an additional layer of fibre demand. As AI inferencing workloads are pushed closer to end users — into carrier edge nodes, enterprise premises, and even base station sites — the backhaul and fronthaul networks connecting these distributed compute nodes must be upgraded accordingly. This is creating new opportunities at the intersection of 5G infrastructure and AI-optimised edge computing, a convergence that fibre companies and telecom operators are both keen to capitalise on.

Industry Outlook: Infrastructure as the New Competitive Battleground

For telecom professionals and infrastructure investors, the message from companies like STL is unambiguous: optical fibre is no longer a commodity — it is a strategic asset in the AI economy. Nations and enterprises that invest aggressively in high-capacity, low-latency fibre networks today will be best positioned to host, deliver, and monetise AI services tomorrow.

The coming years will likely see deeper collaboration between fibre manufacturers, hyperscalers, and traditional telecoms operators as the industry races to build the physical foundation that the AI revolution demands. Standards bodies are already working on next-generation fibre specifications, while governments worldwide are beginning to recognise that fibre infrastructure policy is inseparable from AI competitiveness strategy.

In short, the AI boom is not just filling data centres with GPUs — it is lighting up fibre networks around the world, and the industry is only just beginning to grasp the full scale of what that means.